What are your Borrowing options?

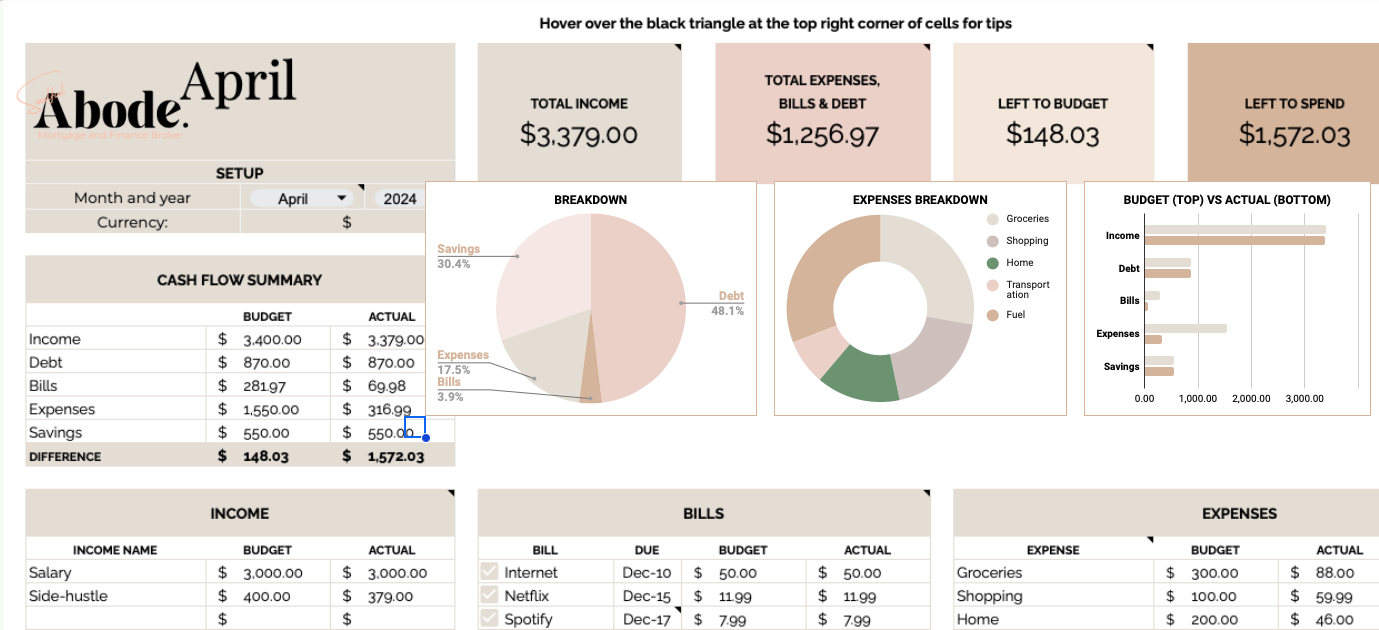

Check out our borrowing calculator below to see how much you can lend.

Start here and explore the many possibilities available for your mortgage needs. Our thoughtful and comprehensive approach ensures that you have access to a variety of tailored lending options specifically designed to meet your unique financial situation. To get started on this journey, we encourage you to book a consultation with Caitlin. During this meeting, she will work closely with you to outline your personal preferences and financial goals, ultimately helping to create a personalised lending plan that suits your needs perfectly. Reach out to us today to take that essential first step towards achieving your ideal mortgage solution.

A deposit, often referred to as a down payment, is a sum of money that a buyer pays upfront when purchasing a property. This amount is usually expressed as a percentage of the home's purchase price. For most home loans in Australia, a deposit of at least 5% to 20% of the purchase price is common.

The deposit serves several important purposes:

Commitment: It demonstrates your serious intent to purchase the property and is often a requirement in the sale agreement.

Secured Financing: Lenders typically require a deposit as part of the application process for a mortgage. It helps reduce the risk for lenders by ensuring that buyers have a financial stake in the property.

Equity: The deposit contributes to your equity in the home, which is the portion of the property that you own outright.

Loan Approval: A larger deposit can improve your chances of securing a loan and may lead to better interest rates, as it indicates lower risk to the lender.

There are various options available for deposit assistance in Australia, particularly for first-time home buyers. These may include:

First Home Owner Grant (FHOG): A government initiative providing financial support to eligible first-home buyers.

Home Loan Deposit Schemes: These programs allow eligible buyers to purchase a home with a deposit as low as 5% without needing to pay Lenders Mortgage Insurance (LMI). In South Australia, you can access offers of as little as 2% deposit. Book with Caitlin to see if you are eligible.

State-specific grants and assistance: Many states offer additional incentives or schemes aimed at helping first-time buyers with their deposits, such as shared equity loans or matched savings programs.

Using a Broker will eliminate the stress and time it takes to research what you are eligible to access. Caitlin will do all that groundwork for you- Book in and start your Abode Journey

Who says property investment is just for the big guys in suits? Not us! Ladies, it’s YOUR time to shine, build wealth, and create the legacy you deserve. Whether you’re dreaming of financial freedom, securing your kids' future, or just proving to yourself you CAN do it—we’re here to help you make it happen.

Starting the journey toward home ownership can feel overwhelming, but breaking it down into manageable steps can help. Here are some key points to consider:

Assess Your Financial Situation: Gather your financial documents, including income statements, debts, and savings. Understanding your budget is crucial.

Determine Your Needs: Think about what you're looking for in a home. Consider factors like location, size, and amenities that matter to you.

Get Pre-Approved for a Mortgage: Before house hunting, speak with a mortgage lender and get pre-approved. This will give you an idea of how much you can afford and show sellers you are serious.

Research the Market: Look into housing markets in your desired areas. Pay attention to prices, trends, and future developments that could affect your investment.

Find a Real Estate Agent: A knowledgeable agent can guide you through the buying process, offering insights and support tailored to your needs.

Start House Hunting: Begin your search, keeping your needs and budget in mind. Attend open houses and take note of what you like and dislike.

Make an Offer: Once you find a home that feels right, work with your agent to make a competitive offer.

Complete Inspections and Appraisals: Once your offer is accepted, conduct necessary inspections and appraisals to ensure the home is in good condition and valued correctly.

Finalise Your Mortgage: Work with your lender to complete the mortgage process, making sure all paperwork is submitted on time.

Close the Deal: Attend the closing meeting to sign documents, make necessary payments, and officially take ownership of your new home.

Each of these steps plays a significant role in securing a mortgage and buying a home. Taking the time to carefully navigate each one can lead to a successful and fulfilling home-buying experience.

Ready to Get Started on Your Homeownership Journey?

At Soulful Abode Mortgages, we’re here to make the process seamless and stress-free. Whether you’re a first-time buyer or looking to refinance, Caitlin is ready to find the perfect loan solution tailored just for you.

Click below to book your FREE consultation today and let’s get you one step closer to your dream home!

Mannum based Broker is currently servicing South Australian clients. Lending can be Australia-wide.

Did our calculator help? Remember these are for general use if you are ready to explore more into your financial journey don’t forget to Book in with Caitlin today

Home Loan Health Checks and Mortgage Refinancing

A home loan health check is an essential and important process designed specifically for homeowners who are looking to ensure they are getting the best possible value and terms from their mortgage. This comprehensive assessment typically involves thoroughly reviewing the current loan terms, interest rates, and various features in comparison to the broader market conditions that may be currently available. The primary goal of this evaluation is to identify any potential savings or benefits that could be realized through the process of refinancing, which may ultimately lead to more favourable financial outcomes and improved financial stability for the homeowner. Get in contact with Caitlin to see if she can get you a better offer or if you feel that your current loan is not serving the same purpose Caitlin is happy to review your options ( Psst… it’s yet again free service)

Key aspects of a Home Loan Health Check

Interest Rate Review: Evaluating whether your current interest rate is competitive compared to market rates can potentially lead to savings. Consider refinancing if rates are significantly lower.

Loan Term Assessment: Analyze the length of your mortgage term. Shorter terms typically have higher monthly payments but lead to lower overall interest costs. A longer-term may ease monthly expenses but increase the total interest paid.

Payment History Evaluation: Check your payment history for any missed payments or late fees. Consistent, on-time payments can improve your credit score and aid in obtaining better loan terms in the future.

Equity Position: Determine how much equity you have in your home. This can affect refinancing options and your ability to take out additional loans against the property.

Debt-to-Income Ratio: Evaluate your debt-to-income (DTI) ratio. Lenders generally prefer a DTI of 43% or lower. If your ratio is higher, you may want to address debt levels or increase income for better financing options.

Property Value Assessment: Keep an eye on local property values. An increase in home value can enhance your equity, while a decline might require adjustment in your financial planning.

Loan Type Consideration: Understand the implications of your current loan type (fixed vs. adjustable rates) and assess if it still fits your financial goals and lifestyle.

Financial Health Check: Review your overall financial situation, including savings, investments, and emergency funds. A healthy financial status can open up more options for refinancing or purchasing additional homes in the future.

Prepayment Options: Look into the terms regarding prepayments. Some loans come with penalties for paying off the principal early, which might impact your strategy for reducing debt.

Future Goals Alignment: Ensure your loan terms align with your long-term financial goals, whether it's upgrading, downsizing, or investing in additional properties.

Itsd very important to conduct a home loan health check Caitlin Helps you to make an informed decision based on your current financial situation and future objectives.